I can be over- or under-invested in PE

5/26/20244 min read

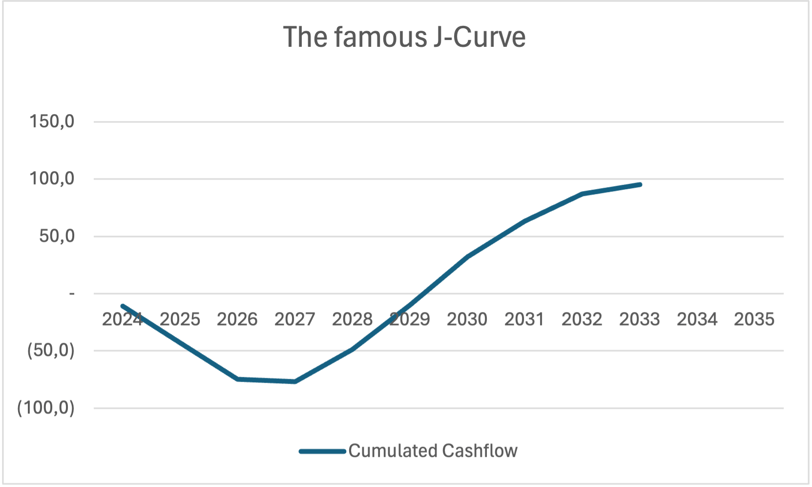

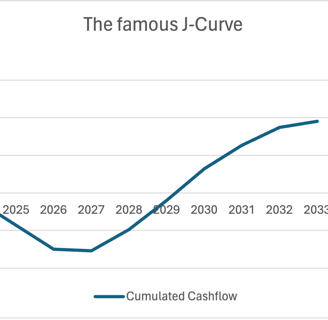

So, the chart above illustrates a J-Curve, under near-perfect conditions. You might initially observe that it doesn’t exactly resemble a “J”. While that’s true, the concept here is to demonstrate that before realizing capital gains, one must be prepared to remain invested for a considerable duration (5 years in this example, with no liquidity, and 6 years before making the first gain).

The chart is based on a fund with the following characteristics :

We have made arbitrary deployment assumptions and anticipate a standard buy-out return of 2x gross, with some deals performing better. However, this team is competent, and there are no write-offs.

The J-Curve is basically just the Cumulated cashflow from the investor's perspective, over the lifetime of the fund. Your cashflow is affected by the capital calls to fund investments, but also by the calls to fund fees.

Some comments on the facts that few people know about GPs and LPs :

- The J-Curve usually does not bottom out at 100% of the LP commitment. Usually, good teams are able to send back money to investors before the end of the investment period. This is because teams need to raise new money in a new fund before they run out of dry powder, as already mentioned. There are other ways to influence the bottom of the J, but more of this in the next post.

- For an LP, given the fact that he is unlikely to deploy 100% of his commitment, it is important to compute a ratio called "PICC" : Paid-in over capital commitment. It can be as low as 50% in some cases ! This is a two-sided sword. It is great, because the fund is more efficient in the handling of its capital calls, but from an LP perspective, in a good fund with a low PICC, he never puts his money at work. If he really wants to invest X, he needs to take a commitment of X/PICC. But PICC, given the macro environment, can increase, and hence the LP will be over-exposed...

- The GP charges fees of 2%. Usually during the investment period, the rate applies to the total fund size. After the end of the investment period, the rate remains at 2%, but is only applied to the remaining portfolio at cost. It must be noted that usually, the GP cannot call for more than 100% of commitments over the lifetime of the fund. Hence, if the GP was not to generate exit proceeds sufficiently quickly, he will not be able to fund his running costs, and hence interests with LPs are aligned beyond the carried interest.

- Usually, the J-Curve flattens 7-8 years after inception of the fund. This is when the carried starts to be paid to the team. The first year, the amount is usually more than 20% of the gains, because the investor pays (or accepts to not perceive) the catch-up after having received the hurdle.

- To provide a broader perspective on the above example : Investors invest €77m, and perceive gross proceeds of € 230m, i.e. a multiple of 2,99x, or a gross capital gain of € 153m. These proceeds generate carried interest and pay fees for a global amount of € 34,7m. They leave ca. 22,7% of their capital gain to the GP. But only € 10m are certain (the management fees during investment period), the rest is performance-related. Talk about aligning interests !

- One last boring element but which the investor needs to bear in mind : he will get quarterly Account statements. These will show a loss at the beginning. Indeed, the fund calls money to invest (which is usually not revalued before the first anniversary of the deal). But the fund also calls the fees, which are, from the fund perspective a cost (he calls it from investors but pays it back to the Manco). In the example above, at the end of 2024, your capital account will show a Gross Asset Value of € 11m, but a Net Asset Value of only € 10m, showing a loss of ca. 9% ! Plus, the fund does not revaluate positively in the first twelve months, but if there were to be bad news, or if valuation principles show that the initial 10m investment needs to be written-down, this will be booked. If the investment (e.g. because comparable listed companies are valued at lower multiples at that year-end) is to be valued € 1m less, you are close to 20% loss in the first year. You need to have strong nerves !

If you are not asleep yet, think about what happens to the investor if he likes the fund (I would, they are giving great returns, especially for a buy-out fund!). The fund, raised in 2024, will be deployed at 70% in late 2026. It will start the next fund-raising process. If all LPs are happy, the next raise can be rather quick, and will usually be closed at a higher level than the previous one.

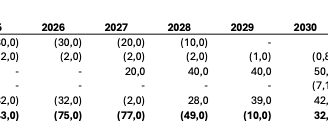

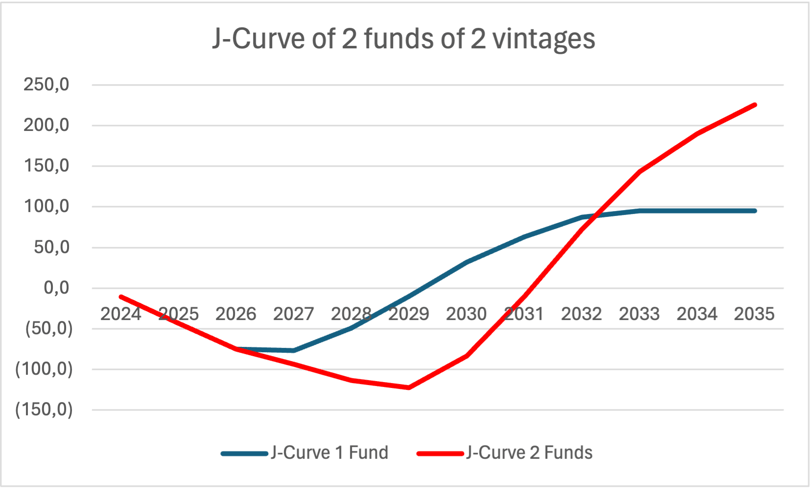

Let's assume that the investor decides to subscribe the same portion to the next fund, but which will be closed at 1,5x the size of the the 2024 vintage, and that it will be closed in mid-2027. This means that the LP "re-ups". He is not growing his exposure, he just keeps his "preferential subscription right". Let's also assume that the Fund has exactly the same terms and conditions, same deployment pattern and the same performance. For the LP, it means that the cash neutral point moves from 2029 to 2031 ! It also means that the bottom of the J-Curve goes down from €77m to €115,5m. But the global PICC (77% at one single fund) is reduced to 49%, because the proceeds of Fund 1 cover capital calls for Fund 2 :

If the next fund is performing as well as the first one, there is obvious interest for an investor to re-up, because he will improve overall capital gains significantly, while not investing significantly more net assets. That is why PE is a long-term game. But it supposes that Funds reach comparable performances through all vintages. This not only depends on the team, but also on the global environment. This is why diversification is adamant !

But more on this in the next post. We hope you have enjoyed this post. Please feel free to react here or write to contact@korafin.com !