The Maze of Private Equity funds and strategies

5/19/20243 min read

If you have made it through our first series of posts and found them interesting, you might be wondering why we discuss pitfalls, risks, but also incredible opportunities and a certain outperformance of other asset classes.

This is primarily due to the fact that, although vast, private equity (PE) is a relatively discreet asset class that aims to flourish outside the public's scrutiny. This is despite the fact that many large players have chosen to list themselves and enter the spotlight.

Firstly, PE is just one category within the larger space of private assets. This includes private debt, infrastructure projects, and numerous niche strategies, such as investing in the financing and outcome of large commercial litigations under arbitrage. We will delve into other asset classes after the end of this series.

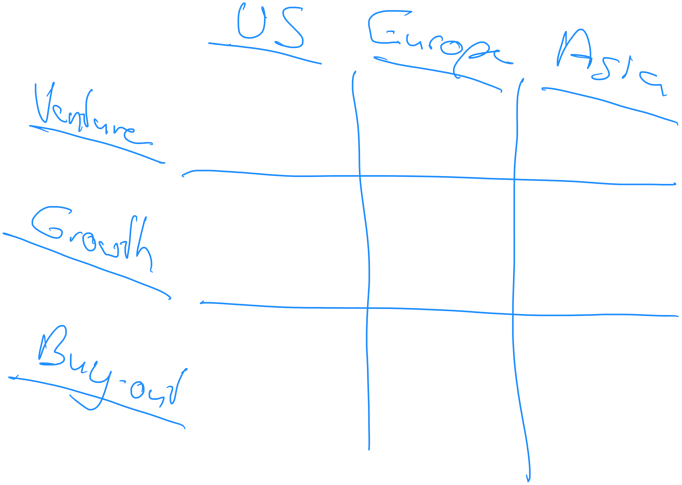

If we focus on PE, there are three main categories: venture, growth, and buy-out. These categories divide the space of investable companies by their development stage and maturity.

Venture is for start-ups that may still be in the idea stage and is the riskiest category due to the many potential issues that can arise.

Growth is for companies that have proven their market exists and that it adopts their product. These companies need additional capital to build their operations in a meaningful manner ("to scale") as they are still too young and uncertain for traditional bankers to trust.

Buy-out is for mature companies that seek new capital to initiate strategic moves, such as restructuring their capital, buying a competitor, or funding large investment projects with a pay-back period that goes beyond what a banker can or is willing to finance alone. Buy-outs usually include a debt component, hence the term leveraged buy-out ("LBO").

There is also a second separation criterion: geography. One significant advantage of PE is direct access to information, but you need to be able to act upon it. There is no point in knowing that a company in Vietnam is facing difficulties if your investment team is based in the US or Europe. Although there are funds that cover all continents, even Blackstone started as a pure US company, not even considering opportunities in Europe. The main reason for this small scale is that you need to be deeply embedded in your market to generate deal opportunities. PE is a relationship business, and all investors sell the same thing: money. Those who succeed are those who can better help their companies develop, which requires proximity, nimbleness, and professionalism, qualities rarely found in large integrated corporations.

In essence, you can create a matrix like the one heading this post. To build a well-diversified portfolio, ideally, you should tick all the boxes, although not necessarily in the same percentage. This is because venture and growth are riskier than buy-out. Additionally, you should not have just one single fund in every box, as you need to diversify the risk.

This may seem complicated, and you may not have the time or contacts to invest in all these funds. This becomes even more acute when we discuss sector diversification, especially for venture and growth but increasingly also for buy-outs. Tech is a vast concept with many sub-sectors, and you cannot be knowledgeable in all of them. The same applies to Healthcare (biotech, genetics, drug delivery, medical devices) and many others.

If you recognize that this is a complex field and that you might need help, there are many consultants of varying size, competence, and interest that can assist you. However, there is an easier way to avoid getting lost: let someone else do the fund selection for you. This is where Fund of Funds comes in. These vehicles raise money from investors and commit to other PE funds that follow a specific strategy. The goal of a fund of funds is to achieve better diversification for you by making a balanced selection of well-performing teams that, in the end, will achieve above-average performances with good risk mitigation. Such funds of funds usually specialize in a given sub-class but cover this asset class globally. Some larger firms have teams specialized in all three maturities and thus cover PE globally. However, you usually need to invest in several vehicles to achieve such global coverage.

This was a broad introduction. In the next post, we will delve into more details about how a PE fund works from the investor's perspective before elaborating later on the best way to select the more meaningful players.

We hope that you will continue reading. Please send feedback here or write to contact@korafin.com !